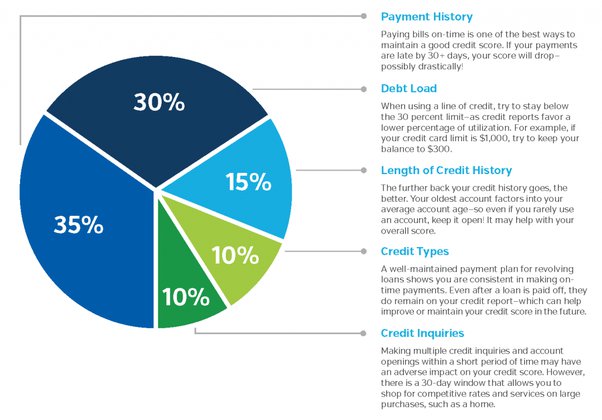

Credit scores can be confusing. But there are ways you can improve your score. Remember to keep your credit clean and not get into credit card or other debt. Asking questions is a great way to learn more about credit. This article will provide information on VantageScore (FICO), and Hard pulls.

Very hard pull

If you are considering applying for a new credit card, you should know that hard pulls can lower your score. Even though most lenders and financial institutions do not make very specific inquiries, they can impact your score. You should understand that only a portion of your score is affected by hard inquiries. These inquiries are often made to confirm your ability to repay a loan, or lease.

Credit card issuers will run a hard check when you apply for new credit cards. Hard pulls can also be done by private student loan and mortgage lenders. If you are applying to rent a unit, your landlord may conduct a hard check. These lenders want to ensure that you are reliable and can repay any loans.

Soft pull

Soft pulls are credit checks that do not require a formal application. Hard pulls are when a lender obtains a client’s credit reports and scores. A hard pull is more detailed and provides a lender with a better view of a client’s credit history.

To compare rates, you may need to apply to at least half a dozen lenders when applying for a creditcard. Each inquiry you make will be considered one inquiry in your credit report. The hard inquiry will not affect your credit score and it will be visible on your report for up two years. However, if your payments have been on time, the soft pull should have very little impact on your score.

VantageScore

VantageScore, an important component of credit scoring, is something you should consider. Your score is determined using five tiers. This can vary based on credit habits and how you use them. Your ability to obtain credit can be affected by your score, whether you are looking for loans or credit cards or apartment rentals. You can monitor your score to help you manage your finances, and avoid costly errors.

Your credit report and information from creditors about your payments are the basis of your score. Your score may vary from one provider to the next because not all creditors report to all three credit agencies.

FICO

First, understand that your FICO credit score is determined by the information in your file at one of the main consumer reporting organizations (CRAs). Information from lenders, collection agents, and court records can all be found in your file. Some lenders do not report to all three agencies. Your Experian report will show the information in your FICO score on the date of the "pull on" date.

Fair Isaac Corporation has developed the FICO credit rating algorithm. The Fair Isaac Corporation was established in 1956. It uses advanced analytics and math to help businesses make lending decisions. It is today one of the most commonly used credit scores by lenders. Lenders in the United States, as well as other countries, can request the consumer's FICO score at the three major credit reporting agency.

VantageScore 3.0

VantageScore 3.0 relies on data from the credit bureaus. This means that your score could vary. This can be due to the way the scores are calculated and the time period when they are calculated. However, the key factors that make credit score different are the same across credit scores. Lenders such as American Express may use other information in order to determine your credit score.

Experian gives you the opportunity to view your VantageScore3.0 credit score online for free. You can also opt to pay for credit reports at major reporting agencies Equifax, TransUnion, and TransUnion.